What Buyers Actually Said: Two Weeks of Vendor Noise vs. Named Evidence

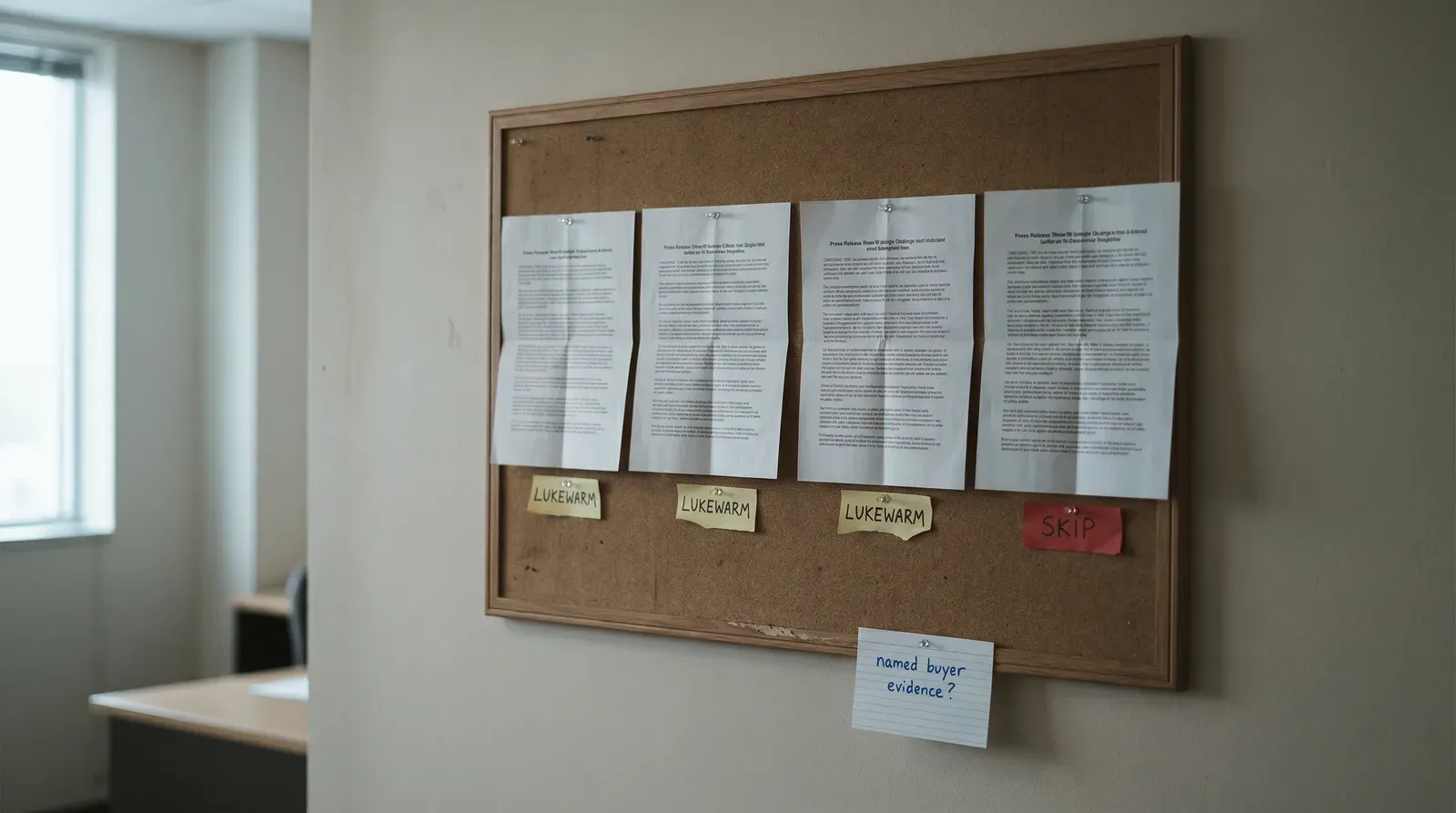

Four W21-W22 announcement clusters scored by named-buyer evidence depth. Three lukewarm, one skip. The contrast that shows where decision quality fails.

Quick decision summary

Five plain-language checks for a go or hold decision

- What claim are we testing?

- Four W21-W22 announcement clusters represent enterprise AI value capture sufficient to justify expansion budgets.

- Who is the named peer?

- KPMG (Bill Thomas, Rema Serafi), Advocate (Andy Crowder), Databricks (Hanlin Tang, supplier not buyer), DeepSeek (no named buyer in window).

- Source strength

- mixed Mixed tiers

- Where this may not apply

- Three clusters carry named participants with mostly intent-and-setup language (lukewarm); one cluster has no named buyer evidence (DeepSeek, skip). Across all four: announcement strength is high, named buyer value-capture evidence is thin to absent.

- Recommended decision

- Hold KPMG (workflow-time evidence is useful, but not enough to fund expansion). Use PwC-Advocate alliance evidence as directional context only. Reject Opus 4.8 for funding decisions (vendor cost input, not buyer outcome). Reject DeepSeek (no named buyer in this window). Use one minimum proof rule for all four clusters: named buyer, before-and-after metric, and one clear business lever.

Corrected 2026-05-31: cluster #2 below collapsed two distinct PwC announcements (May 5 PwC-OpenAI, May 14 PwC-Anthropic) into one and missed the named operational metrics published on May 14. The corrected follow-up verdict is in: PwC’s Second Announcement Had the Metrics, My First Verdict Missed Them. The rest of the baseline below stands as the May 30 snapshot.

Vendor messaging was loud in W21-W22. The buyer record was not.

In the last two weeks, four announcement clusters dominated AI feeds: KPMG-Anthropic on May 19, PwC-Advocate Health on May 14, Opus 4.8 with Databricks framing on May 28, and the continued DeepSeek release wave. If you only tracked announcement volume, this looked like a broad value-capture moment.

If you track named, attributable buyer evidence, the picture is narrower.

This baseline uses one discipline and does not move the goalposts: for each announcement, did a named buyer go on the record about value captured, what exactly did they say, and where are they silent? Silence is data.

1) KPMG-Anthropic (May 19)

Vendor narrative: workforce-scale rollout and responsible AI operating posture.

Named on-record voices: Bill Thomas (KPMG), Rema Serafi (KPMG), Ethan Burris (UT Austin McCombs, included in announcement context).

What was said:

- Rema Serafi made the most concrete workflow claim in the published material, describing a tax-regulation agent build that “used to take weeks now takes minutes” inside Digital Gateway.

- Bill Thomas and the broader KPMG framing emphasized scale, governance, and responsible deployment intent.

- Ethan Burris appeared as a named external voice in the launch context.

Buyer evidence depth:

- Value-adjacent signal exists: weeks-to-minutes is operationally meaningful.

- Named buyer outcome metrics are still thin: no disclosed before-and-after customer metric, no published cost-to-serve delta, no customer-facing quality metric.

Verdict: lukewarm.

Why: this is stronger than generic AI partnership language, but it remains mostly operator-side narrative plus one strong internal workflow claim, not broad buyer-side value capture evidence.

2) PwC-Advocate Health (May 14)

Vendor narrative: scaled deployment, training expansion, and cross-function transformation claims.

Named on-record voices: Paul Griggs (PwC), Andy Crowder (Advocate Health).

What was said:

- Andy Crowder was on record in the announcement as the named client voice.

- The public framing emphasized strategic intent and expected impact from expanded AI deployment.

Buyer evidence depth:

- Positive signal: a named client appears in the public record, which is already better than many enterprise releases.

- Core gap: outcome disclosure is limited. The record in this window does not provide a named buyer before-and-after metric set for cost-to-serve, throughput, or customer-felt functionality.

Verdict: lukewarm.

Why: named buyer participation is present, but this is still intent-forward rather than value-capture-forward in public evidence.

3) Opus 4.8 with Databricks framing (May 28)

Vendor narrative: better model performance and stronger economics.

Named on-record voice: Hanlin Tang (Databricks).

What was said:

- Hanlin Tang stated Opus 4.8 in Genie ran at “61% cheaper token cost than Opus 4.7.”

Buyer evidence depth:

- This is a clear economics signal.

- It is not yet a named buyer value-capture disclosure. Token efficiency is an input to value, not proof of customer outcome movement.

- No named end-buyer in this window publicly disclosed post-deployment customer metrics tied to that cost improvement.

Verdict: lukewarm.

Why: credible technical-economics evidence is present, but named buyer outcome evidence is still limited.

4) DeepSeek release wave (W21-W22 context)

Search scope for this absence claim: a 60-day scan of the publication’s tracked named-buyer set (regulated and large-enterprise operators publicly identified in earnings calls, vendor press releases citing specific buyers by name, conference Q&A transcripts, and analyst-published case studies). The verdict below rests on what was not found inside this set; widening the set may surface evidence.

Vendor narrative: capability momentum and high visibility in model-release discussion.

Named on-record buyer voice in this window: silent.

What was said by named buyers:

- Silent.

Buyer evidence depth:

- Significant announcement and discourse volume.

- Near-zero named buyer evidence in the last 60 days in this vetted set showing value captured in production customer operations.

Verdict: skip.

Why: this is the strongest contrast case. The market signal is loud, but named buyer evidence is sparse. Treating this as proven enterprise value today would be vendor-amplification behavior.

What The Contrast Actually Shows

Across all four clusters, the same pattern repeats:

- Announcement strength is high.

- Named practitioner attribution varies.

- Named buyer value-capture evidence is mostly partial, with DeepSeek close to absent in this source set.

This does not mean the underlying work is weak. It means the public buyer record has not caught up to the scale of supplier claims.

That distinction matters because decision quality fails at exactly this boundary. Teams treat deployment intent as delivered value, then discover six months later that no customer-facing lever moved in a measurable way.

Monday morning rule for CX executives: no expansion decision without one named before-and-after metric mapped to one lever - cost-to-serve, capacity reallocation, or product functionality.

The practical rule for operators and buyers remains straightforward:

- If the announcement gives named buyer before-and-after metrics, treat as compelling.

- If the announcement gives named participants but mostly intent and setup language, treat as lukewarm.

- If named buyers are silent, treat as skip until public evidence appears.

W21-W22 lands as one lukewarm cluster repeated three times, plus one skip case that clarifies the standard. DeepSeek is not the only example of announcement-evidence divergence, but it is the cleanest one in this two-week window.

If this baseline is wrong, the correction path is simple and public: named buyers publish attributable metrics, and the verdict changes.

If no named buyer metric is published, treat the claim as a communication signal only, not an operating signal for budget or rollout scope.

Until then, silence is not neutral. Silence is a negative evidence signal.

Decision line for the next funding meeting (one rule per cluster)

For a delivery owner triaging these four clusters against this quarter’s portfolio defense:

- KPMG-Anthropic: hold. Workflow-time evidence supports the thesis; portfolio-aggregated headcount or margin evidence does not yet exist. Do not cite in funding defense without the trigger metric.

- PwC-Advocate Health: see the corrected re-audit. The alliance-level evidence on May 14 is compelling for the class of deployments (underwriting, security, HR, COBOL). The Advocate-specific verdict stays lukewarm until Advocate publishes before-and-after numbers. Cite the alliance to support a hypothesis; do not cite Advocate-specific to support a renewal.

- Opus 4.8 with Databricks framing: reject as funding evidence. Token-cost claims are vendor-side inputs to value, not outputs. Use only as a cost-model assumption in pricing.

- DeepSeek release wave: reject. No named-buyer evidence in the window. Treating model-release coverage as proof of enterprise value is the pattern the publication exists to call out.

One rule per cluster, all four anchored to the same standard: named buyer + before-and-after metric + measurable lever. Anything short of that is a communication signal, not a funding signal.